The upcoming tax cuts, effective July 1, 2024, have been generating significant buzz. Beyond simply increasing your disposable income, these cuts present an excellent opportunity for homeowners to shorten their mortgage term and reduce the total interest paid.

Here’s how you can leverage the new tax changes to your advantage:

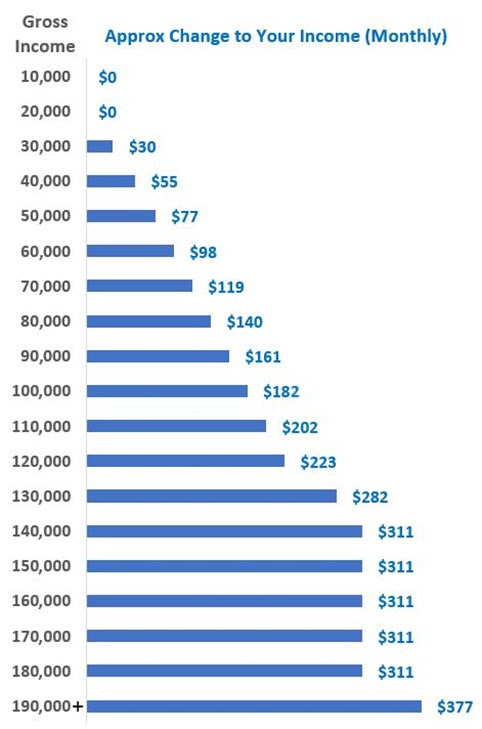

Understanding the Tax Cuts

The stage 3 tax cuts primarily benefit middle-income earners by merging the 32.5% and 37% tax brackets into a single 30% bracket. This means if you earn between $45,001 and $120,000, you’ll pay a lower tax rate, resulting in more disposable income. Additionally, the top tax threshold is being raised, providing tax relief to those earning above $200,000.

For instance, the average Australian taxpayer earning $92,000 annually is set to receive an extra $161 per month. While this might not seem life-changing, redirecting this amount towards your mortgage can significantly impact your loan term and interest payments.

The Power of Small, Consistent Contributions

An additional $37 per week might not seem substantial, but when applied consistently to your mortgage, it can work wonders. Every extra dollar you pay helps chip away at the principal balance, reducing the amount of interest accrued over time.

How Much Could You Save?

The exact amount you save will depend on your income and mortgage details. Here’s a simplified example to illustrate the potential savings:

- Monthly Extra Contribution: $161

- Total Interest Saved: Significant over the loan term

- Loan Term Reduced: By several years

Turning Your Tax Savings into Mortgage Magic

Instead of spending your tax savings on luxuries, consider redirecting them towards your mortgage. Here’s how:

- Increase Your Regular Repayments: Even a small increase in your monthly repayments, such as an extra $50 or $100, can significantly reduce your loan term and total interest paid.

- Make Lump Sum Payments: If you receive a sizable tax refund, consider making a lump sum payment towards your mortgage. This can shave years off your loan term and save you a substantial amount in interest.

- Refinance to a Lower Rate: Use this opportunity to review your current home loan and potentially refinance to a lower interest rate. This can further amplify the savings from your tax cuts.

Additional Considerations

- Offset Account: If you have an offset account linked to your mortgage, depositing your tax refund into this account can further reduce your interest payments.

- Debt Consolidation: If you have other debts, such as credit cards or personal loans, consider consolidating them into your mortgage. This can help you save on interest and simplify your repayments.

- The Mortgage Cliff: If you’re nearing the end of a fixed-rate loan period, the tax cuts can help offset the potential increase in repayments when you switch to a variable rate.

While the July 2024 tax cuts might not result in a massive windfall for the average Australian, they offer a valuable opportunity to make a positive impact on your mortgage. By consistently redirecting your tax savings towards your home loan, you can gradually reduce your loan term and interest payments.

Remember, every little bit counts. Even small, consistent contributions can make a big difference over time, bringing you closer to financial freedom and a mortgage-free future.

Ready to maximize your tax savings and reduce your mortgage? Contact us at 1300 952 286, email [email protected], or visit www.boanco.com.au for expert guidance tailored to your financial goals.